Entrepreneur’s Guide to Fundraising Decks

A fundraising pitch deck is unique to a company and to where that company is in its lifecycle. Core innovations are different. Teams are different. Market opportunities are different. Funding rounds and investor types are different. So, fundraising decks must be highly attuned to those differences.

Even so, there are common elements to successful pitch decks. The following are some archetypal slides we feel can help most focused ultrasound-related companies craft an effective pitch deck. For each slide type, we make suggestions about what kinds of content should be on it, and why. And we give illustrative examples, some from real-world use cases.

The FUS Partners program hopes you’ll find this helpful and stands ready to help you in your entrepreneurial journey however we can.

Table of Contents

- General Principles

- The Title Slide

- Summary Highlights

- Team

- Core Innovation and IP

- Market Opportunity

- Business Model

- Go To Market

- Competitive Landscape/Differentiation

- Regulatory Strategy

- Reimbursement Strategy

- Development Pipeline

- Risks

- Summary Financials

- Summary Wrap-up

1. General Principles

A pitch deck is unique to a company, but there are common elements to successful ones. The following are some archetypal slides that can help craft an effective pitch deck. For each, you’ll find what should be on each slide and why, as well as examples from real-world use cases.

First, some general principles:

Build the Investment Case

Most investors must build an investment case for your business. Schematically, it may look a lot like this (for almost any business);

Market Need → Core Innovation → Product → Business → Competitive Differentiation → Scale-up → Profitability → Exit

If you can lay that sequence out clearly — and demonstrate that capital out is likely to exceed the capital invested — 90% of the battle will have been won.

Tell A Story

- People respond innately to stories. Your deck and your pitch should first and foremost tell a story.

- While we will suggest some slides that are usually necessary for an effective fundraising deck, merely including them will not do the trick.

- You must capture the investor’s imagination with a differentiated story that helps them build their own investment case. Keep in mind that most professional investors will see 1,000 to 1,500 business plans per year. That’s five per day. Your story needs to be clear and compelling, not to mention differentiated, to stand out.

- Your early data are great, yes. Your device has better performance across attributes x, y, and z — awesome. None of it matters unless you develop the narrative around why it meets a quantifiable market pain point and is so much better that it will displace the current solution or prompt a new buying behavior.

Use Headers To Tell the Story

- A reader of the deck should be able to get the gist of your story from reading just the headers of each slide.

- Headers must explain the significance of what’s on the slide — not simply state what is on the slide.

- A good deck will have a sequence based on the above investment case logic, and the slide order and headers should reflect it. Headers should be the “Cliff Notes” of your story.

Use Appendices Liberally

- Any slide or idea that doesn’t obviously and critically build the investment case belongs in the appendix.

- There should be just enough slides in the deck to make the logical sequence clear, but no more. Make liberal use of appendices so your pitch deck is lean and mean.

- Ideas that aren’t critical to the sequence but which are likely to be referenced as supporting material should go in the appendix.

- It’s okay for the appendix to have 2x or 3x the slides of the main deck.

Don’t Confuse Good Tech and Strong Intellectual Property with a Good Business

- Technical founders often misunderstand that strong intellectual property (IP) and/or strong technology are necessary but completely insufficient to have a good business.

- Charts and graphs of your scientific data or your device’s technical attributes are (probably) necessary but insufficient.

- Start with a clear assertion about why the ultimate buyer (as distinct from the user) will buy what you are selling.

- The deck then supports that assertion.

Use Different Materials and Different Versions for Each Stage of Fundraising

During the fundraising journey you will benefit from having the following versions of your core story:

- a one-paragraph email teaser for the initial outreach to investors to see if there’s any point in sending a deck

- an overview deck for those investors who respond positively to that email or a call.

- a longer overview deck that is subject to a non-disclosure agreement (NDA) for those investors who respond positively to the initial overview deck.

2. The Title Slide

On the Slide

- Company Name

- Tagline (if any)

- Use a vague date (i.e. “2021” or “2H21”)

- Contact info

Commentary

The cover slide is straightforward: company name, tagline, and contact information.

This is the only slide in the deck where you are not explicitly helping your audience build the investment case (but the investment case logic is above anyway just to remind you how crucial it is).

Graphic

If you have a good logo or a relevant graphic, use it. Otherwise, simpler and cleaner is always better.

Tagline

Consider a tagline that frames why the company’s work is important and/or different, not merely what it does. Specificity is better than generality.

Date

Do not put a specific date on introductory decks, as investors can use it to identify changes in your claims and plans over time. Later, in serious due diligence, when you might be exchanging multiple decks, it’s okay.

3. Summary Highlights

On the Slide

This example lacks information on team, core innovation, product, market, and business model, but it does a good job laying out the context for the financing need.

Team

This slide should include a sentence or two on your team to establish credibility and fit. Why this team for this opportunity? Use thumbnail photos and logos of relevant previous companies or universities if there is room to reinforce your assertions of fit and credibility.

Core Innovation(s)

Include a sentence or two on your core innovation — the competitive advantage available only to your company, whether protected by patents or know-how. This is what gets commercialized. It is not (yet) the product or the business model. The core innovations give the company optionality, should pivots become necessary or advantageous.

Product(s)

There should be a sentence or two on the products enabled by the core innovations and, perhaps, the sequence in which those products will be released. You should also include a pipeline of other products available with further R&D.

Market Opportunity

Include a sentence or two on the addressable market opportunity available to the products outlined above. It’s fine to show the total market size and growth rate, but be sure to summarize the:

- Total Available Market (TAM) — The total market demand for a product or service.

- Serviceable Available Market (SAM) — The segment of the TAM targeted by your products and services which is within your geographical reach.

- Share of Market (SOM) — The portion of SAM that you can reasonably expect to capture.

Business Model

Be sure to describe the way(s) the company will commercialize the products and attack the market opportunities outlined above, broken down by product and/or market opportunity, as needed.

Financing Needs

Finally, include a sentence or two outlining the current capital need (what you’re raising this round) in the context of the total capital need. The total capital need is what it will take to get to some meaningful state of cash flow independence.

4. Team

On the Slide

This example establishes credibility with former employment and university affiliations but could benefit from also showing how the team will be built out (i.e., an org chart with open roles).

The primary purpose of the team slide is to establish credibility and fit. Why this team for this opportunity?

Show the Core and Extended Team

- Core Operating Team

- Current

- Near Future

- Scientific Advisors

- Board of Directors

- Investors

- Consultants and other Advisors

Commentary

- Use thumbnail photos and logos of relevant previous companies or universities – if there is room – to reinforce your assertions of fit and credibility.

- Show depth of talent and ability to execute.

- Make sure the reader of your deck clearly understands the track record.

- Displaying support from Key Opinion Leaders (”KOLs”) and other key partners bolsters credibility.

- If there was ever a time your parents told you not to brag….this isn’t it!

- Include technical or science founders but make sure you cover the business roles fully.

- Include Founder-Market fit.

5. Core Innovation & IP

On the Slide

Articulate your Core Innovation(s).

- A innovation can be a novel compound, technology, or even business model.

- Core innovations drive products which solve market problems. Make sure you take every opportunity to show these connections.

- Avoid any hint that you have created a “solution in search of a problem.”

Show How the IP Protects the Innovation and the Business Model

- Core innovations drive products which solve market problems. Merely having protected IP is usually necessary but insufficient.

- Show how the IP protects the innovations and how, therefore, your business model has an unfair advantage in the market for some period of time.

Show How the Future IP will Protect and Extend the Business

- Core innovations drive products which solve market problems. New innovations should drive new products to solve new market problems and/or protect your business from competition.

- Don’t just list inventions that you plan to patent. Make the connections to the business.

Commentary

- Don’t forget to ground this slide in the investment case you are building for your reader.

- Make sure your header outlines the significance of what’s on the slide, instead of just stating what’s on the slide.

6. Market Opportunity

On the Slide

- Market size and growth

- What is being replaced and why?

- Which attributes will make users change their buying behavior? Over what time horizon?

- How will the company execute on the opportunity?

Market Size

- Total Achievable Market (TAM): The projected total size of the market being addressed and growth rate.

- Serviceable Available Market (SAM): The segment of the market the technology can corner and its growth rate.

- Share of Market (SOM): a realistic percentage of the SAM, grown at a reasonable rate each year given the resources of the company.

Market Opportunity

Often a market can be too mature and crowded to break in. Or the market doesn’t even exist yet, and there isn’t a sufficient force or trigger to create a new market. A winning investable idea demonstrates an opportunity and a business with defensible advantages that can serve that market. Answer these three questions:

- What has changed such that now is the time to enter an existing market or create a new market?

- What is the ‘proprietary rationale’ that positions the product/service to enter or create that market?

- What are the barriers to market success and how will they be addressed

Existing Markets

In entering an existing market , show why you can displace current players and why now is the right time to do so. The burden of proof is to show that you have something so compelling it will disrupt the status quo.

New Markets

When creating a new market, show why the opportunity necessitates the creation of a new market, why this hasn’t been done before, and why now is the right time. The burden of proof will be that the market exists, that the proposed product/service will address the market needs, and that there will be demand for the product/service.

Competitive Advantages

- The proprietary rationale is how the product/service is positioned uniquely to take advantage of the opportunity.

- A technical edge indicates a unique technology that is vastly better than previous technology or that of competitors.

- A counterintuitive point of view is a unique perspective that few others share. Most people believe what you’re doing can’t be done, but you have a solid rationale for why it will work and why the conventional wisdom is ripe for being overthrown.

- Do you have a novel model for selling into a new or existing market?

- Are you the first to put technological advances to work to meet a specific need?

- Are there changes in user behavior that are addressed by the technology/service?

- Barriers are what make an idea interesting and valuable. If there weren’t barriers, anyone could solve the perceived problem and probably already would have. Examples include:

- Technical

- Regulatory

- Reimbursement

- Getting people to change established behaviors

- Getting the product into the market

Market Structure and Entry Strategies

- Is there a subsegment of the market that you can corner right now? This could be the share of the market that’s closer to your location or that you can reach more easily.

- What’s the market share of your competitors? Do you know roughly how many sales or customers that your competition has? Compare your business only with competitors of a similar size.

- What’s one to five percent of your market size? Computing this portion of your total market size will give you a conservative enough estimate of your own potential pool of customers.

- The total achievable market (TAM) is a number that represents the total demand for a product or service. This is the top level number. The TAM might be geographically bigger than your business can reach right now. The number may cover people only mildly interested in the product or service or whom you identified as possible target groups based on demographics alone. This number could be the total revenues in a particular industry – it’s the “big” number.

- The serviceable available market (SAM) is a portion of the TAM that is targeted by your product your service. Usually this is in a more immediate geographic reach, or with some other level of targeting to make it a focused segment of your market. This is where we start to narrow things down.

- The share of market or serviceable obtainable market (SOM) is the portion of the SAM that you can actually or feasibly capture. This can be shown as a percentage of the SAM, for example: we can win 10% of the market share in the next two years. The SOM is an interesting number because it takes into account the fact that you are not the only solution your customer has for your product or service. No company in the world (except for monopolies) have 100% of the market. So to make it seem like you expect to get 100% of a market would be completely incorrect.

7. Business Model

On the Slide

Your business model is fundamental to how you run your business. It is important that investors have a clear understanding of what you are selling, how you are selling it, and the value provided to your customers. To demonstrate the viability of the company’s business and the business case for investing, you must understand your customers needs, how to solve for them through an effective go-to-market strategy, and how that strategy translates to shareholder value creation. This slide offers you the opportunity to thoughtfully outline how the company will create value, setting the audience up for future slides that will address the strategy it will pursue to be successful.

How Value is Created

Value is created when your output is more than your input. A company has various stakeholders – investors, customers, employees, etc. Ideally, a company creates value for each group of stakeholders. At the very least, a company must demonstrate that it will create value for its prospective investors.

How Value is Captured

By solving for an unmet need – or providing a better solution than what already exists – a company captures value for its customers. However, to capture value for itself, the benefits received must exceed the efforts and resources expended in delivering a customer solution. What resources are needed to design, develop, manufacture, market, sell, and support your product? How will you price your product and services? Will you charge your customers based on the value you create for them, or will you take a different approach? What is a customer’s payback period, and how does that translate to your company’s profitability and return on investment (ROI)?

Who is the Buyer?

To demonstrate value to your customers, you must get to the person or group who holds the power – and controls the budget – in making the ultimate purchase decision for your product. Investors want to see that you have a clear idea of who the buyer is and what drives their decision making. To complicate matters, the buyer will also include the payor, as ultimately the product purchased will involve claim submission and reimbursement. For example, it’s likely that focused ultrasound equipment isn’t directly reimbursable by insurance. However, it’s important that the procedures performed on and the consumables used with respect to the equipment are reimbursable.

Who is the User?

As often is the case in healthcare, the buyer of the product is separate from the end user. It is important to understand the dynamic between these two stakeholders, the implications and how they might differ across types of provider and payer.

What Partners are Necessary?

As a young company, what resources might you lack that create obstacles to success? Do you have distribution? Do you have equipment servicing capabilities? Is your supply chain resilient? Thinking through your partner strategy and identifying gaps that you intend to fill is important and shows investors that you understand what it will take to scale as your business grows.

Business Model Examples

Equipment

Do you intend to sell equipment outright or lease it? If the latter, how will you fund the manufacture and upkeep of your installed base? Are there third-party lessors/lending companies that would have an interest in this nascent market? What will be the terms of such an arrangement? Who will bear the risk if a customer defaults on payments?

Revenue/Risk Share

Instead of selling equipment to a provider, do you instead intend to share in the reward and risk of the future revenue-generating capacity of your product?

Equipment-as-a-Service or Rental

Would it be valuable and more appealing to your customers to offer your equipment on a subscription basis or as a rental? If so, how will you provide the support needed in the event your equipment falters? Will you have a footprint of technicians placed in the areas of your installed base?

Consumables

Does your company sell products needed to perform each surgical procedure? If so, how are you or do you intend to work with equipment manufacturers to ensure adequate distribution and placement of your product?

8. Go To Market

On the Slide

The Go-To-Market slide articulates a crucial link between your company’s core innovation, the product created from that core innovation, and the business model that takes that product to market.

Market Structure

This slide should explain market structure (who is using the product, who is making the buy decisions, what solutions must be displaced, etc.) and how the business model and team are well-suited to work within that market structure.

Product, Distribution, Regulatory

A complete go-to-market plan will encompass the development of the technology into the product or service but also address the requirements for marketing and distributing it, as well as the regulatory and reimbursement strategies involved for each.

Key Partnerships

Most startups rely on one or more key partnerships to produce, market, or distribute the product or service. Be sure to articulate the nature of those partnerships and how value is created and shared by the partners. Explain what (if any) leverage your company will have in those partnerships and the sequence in which those partnerships would need to be developed.

Business and Financial Model

The GTM slide should tie directly to the financial model: the magnitude and timing of the resources required to execute the go-to-market strategy should all show up in the financial model.

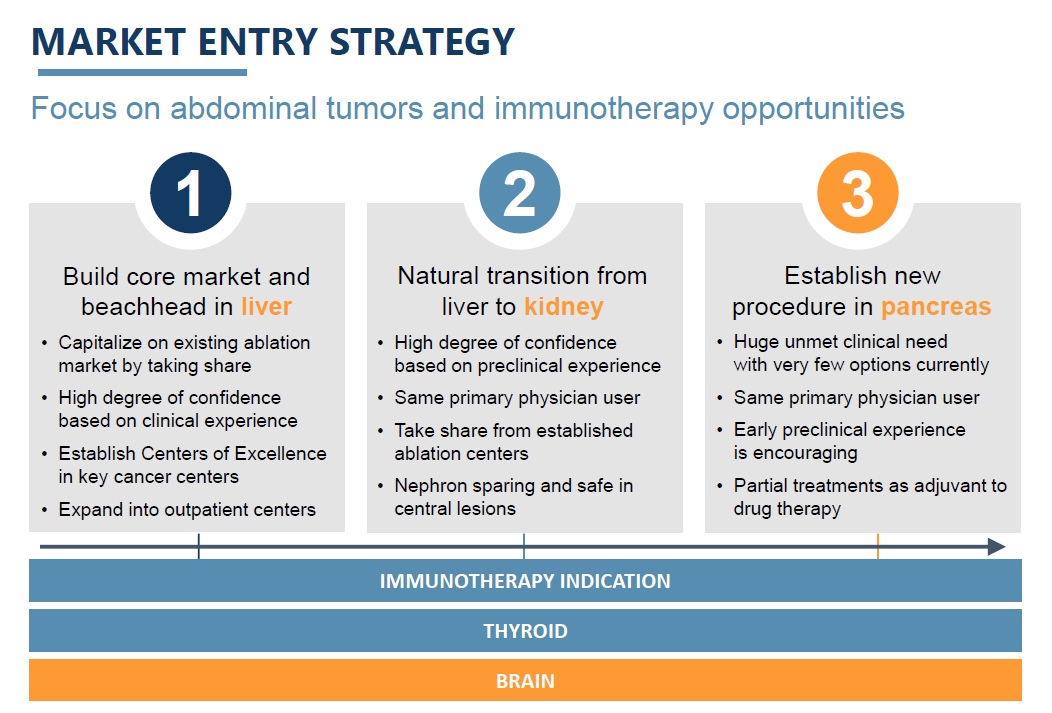

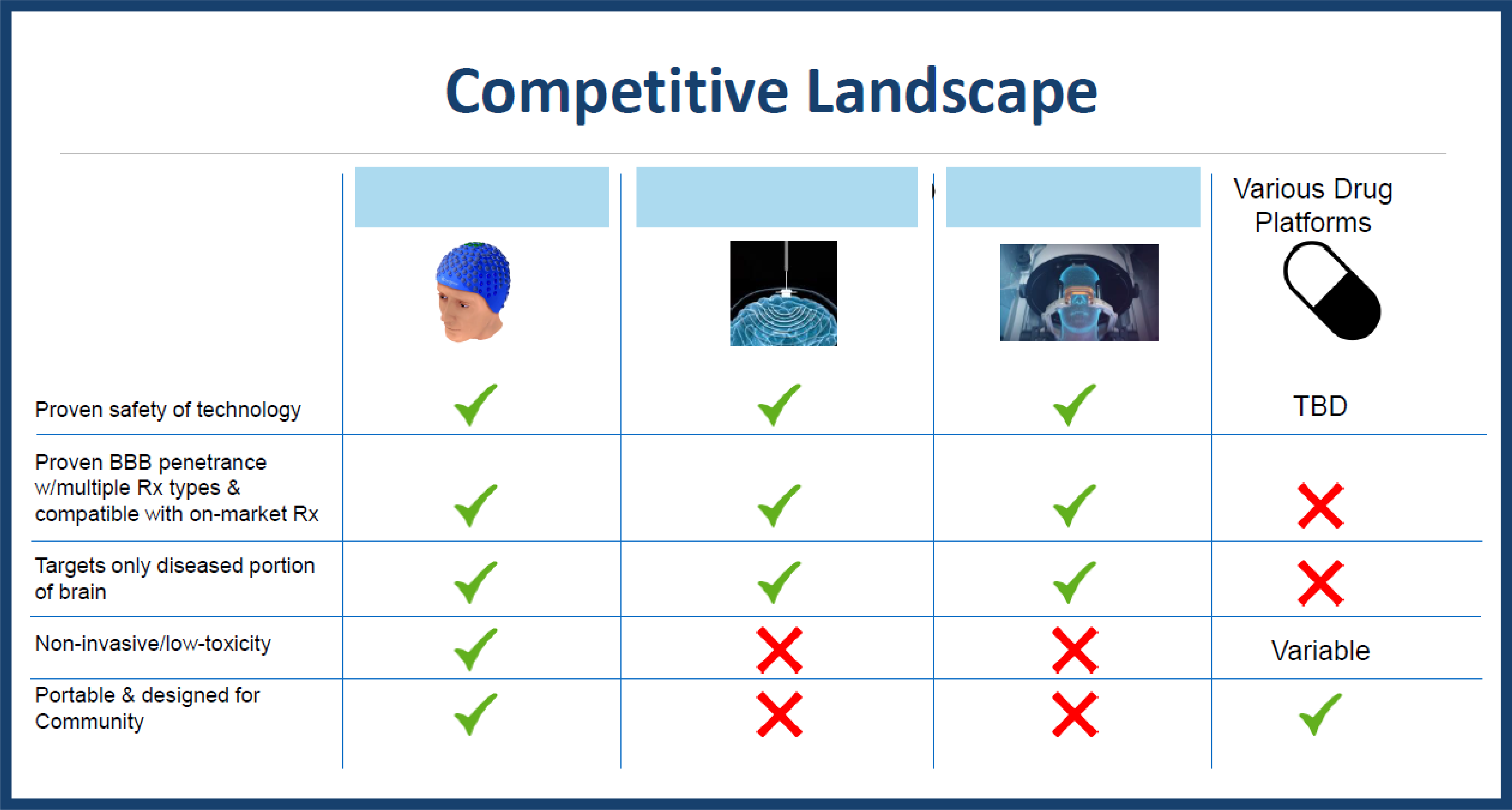

9. Competitive Landscape / Differentiation

On the Slide

This example shows the advantages over the competition — but doesn’t make clear why those advantages are decision-changing for the buyer. Always show why an advantage matters to the buy decision.

The competitive landscape is an opportunity to demonstrate a few critical things:

- that you understand the market you serve

- that you understand who else serves that market — i.e. your competitors

- that you understand how you are differentiated from your competitors

Characterize the Market

- Remind your audience of the market structure. This puts you and your competitors in context.

- Remind your audience of key partnerships. This is one way you will diferentiate.

- It’s okay to have some overlap with the go-to-market slide and others. It will reinforce the logic of the investment case.

Characterize Your Competition

- Even in an un-served or under-served market you have competition. It may come from internally developed solutions.

- Be sure to characterize your competition honestly. Your audience (the investor) will do their due diligence. If you deliberately omit or underplay the competition, the investor may worry that you don’t fully understand them — or worse, that you’re not honest.

Connect Differences to the Buy Decision

- Be sure to show why competitive differences matter to the buyer’s decision. Merely having a different attribute is irrelevant if it doesn’t contribute to the change in decision-making.

- Outline as many relevant decision-changing differences as you can, e.g., cost of CapEx, cost of consumables, time savings, overall ROI, inpatient/outpatient, invasive/noninvasive.

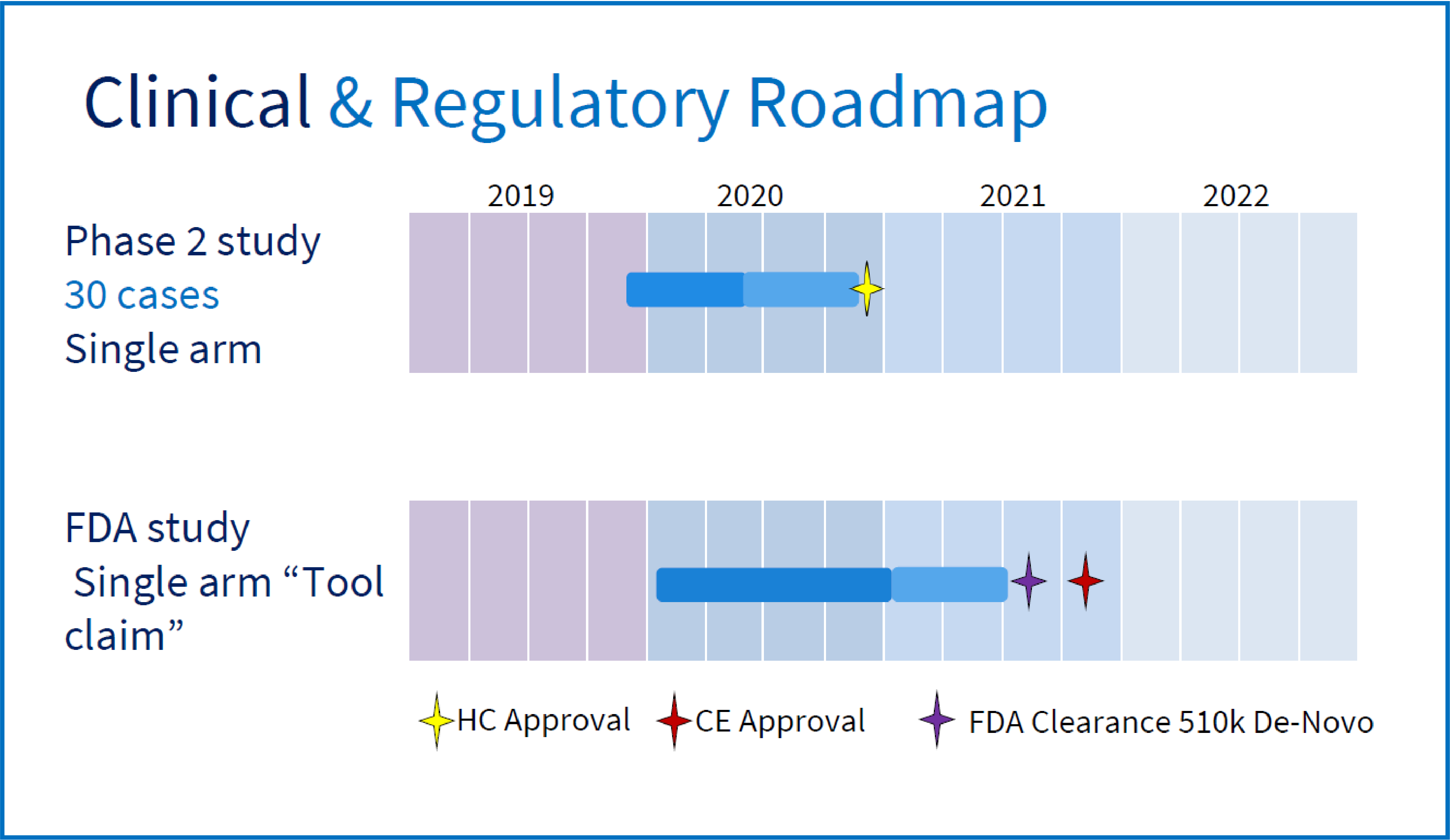

10. Regulatory Strategy

On the Slide

Regulatory authorization is required to bring a product to market. On this slide, detail the path to be taken, the time it will take, the possible hiccups that may be encountered along the way.

Country by Country

The regulatory approval process varies from country to country and from product to product within a given country. It is prudent to explore all geographic regions prior to deciding on the regulatory strategy on which your fundraising is based. It may be that applying for approval first outside the US is the prudent path forward, especially if an easier approval path outside the US will allow earlier market entry and more robust and affordable data generation that then can be used for US submissions. (The FDA is much more receptive to the use of international data than it was a mere five years ago.) This may also be the case if the principal sources of investment come from outside the US, for instance from China.

This example shows some nice detail about the types of studies the company intends.

Optimal Pathway Strategy

While regulatory authorization is a given and universal prerequisite for the sale of technology in the US, the optimal regulatory path for a company may not always be apparent, especially given the impact the decided path will have on the timeline for commercialization. A 510(k) requires the least amount of time and the least amount of clinical data – bench safety data is usually sufficient. A de Novo grant, while often requiring clinical data on short-term side effects, does not require clinical evidence of disease control and therefore can be submitted after a short period of patient follow-up. A PMA is the most costly and lengthy given its need for a clinical trial complete with disease control outcome data that may require years to acquire, but it provides two things the other paths do not; a disease-specific marketing claim and data of the type that may be of value for guideline inclusion and subsequent favorable coverage decisions.

Options

The FDA also has other regulatory pathways that provide reprieve from many of the time-incurring requirements of the standard paths. For instance, the Breakthrough Devices Program speeds up the assessment and review of the technology and provides a prioritized regulatory review.

When it comes time to make coverage decisions, the clinical data acquired as part of a PMA may be sufficient for inclusion in guidelines, a prerequisite for most coverage decisions, while the data acquired for a 510(k) or even a De Novo submission most likely would not reach the bar required for guideline inclusion. Thus, while the cost of performing a PMA is significant and is borne upfront when investor capital is most expensive, it may prove ultimately to be less costly than the revenue loss incurred while waiting for clinical evidence from early adopters of the technology to be published and used to support guideline inclusion.

Figure it Out Early

The importance of making the right regulatory path decision early in technology development cannot be overemphasized. On the one hand, if a PMA is submitted where a 510(k) would have been sufficient to realize all market objectives, many years and multiple millions of dollars may end up being wasted, with those additional years and cost at the front end where investor dollars are the most expensive, leading to increased dilution. On the other, finding out late in the game that a PMA would have proved more fruitful than a 510(K) when it comes to realizing reimbursement coverage will add cost and time at the back end that may end up being greater than the cost if incurred upfront and may cause significant dissatisfaction among the investor pool.

Measure Twice, Cut Once

In many cases, where uncertainty about the correct regulatory path to take exists, a meeting with the FDA prior to electing any regulatory path may be worthwhile. However, once a recommendation is made by the FDA, a company is pretty much stuck following that path. On some occasions, adopting a path and then working with the FDA after the fact to make that path work may make more sense, especially if there is a grey line between the various filing options.

Contingency Planning

Finally, and regardless of the regulatory path chosen, it is important that aspects of the clinical and regulatory development plans that are at risk to incur delays are identified, with ‘cushions’ built into timelines and fundraising plans to account for them. For instance:

- The FDA may designate a device to a PMA pathway whereas the company was expecting a 510(k).

- The company may incur delays in obtaining investigational device exemption (IDE) approval for their clinical trial or securing investigational review board (IRB) approval at one or more of the institutions slated to participate in the trial.

- The FDA may require a trial sample size larger than the one the company originally anticipated and budgeted for.

- Recruitment of patients to participate in the clinical trial may go slower than originally planned.

- The occurrence of a major adverse event may require suspension of patient recruitment until the adverse event can be shown not to be caused by the device.

- The FDA may require additional bench or laboratory testing as part of its review of a 510(K).

- The FDA may require additional reprocessing validation runs which are in turn dependent on the availability of testing laboratories to perform the required analysis.

- The clinical environment may change during the regulatory process.

It is highly likely that at least one of these “hiccups” will be experienced with any device submitted to the FDA. Failure to build contingencies into the funding requirements and commercialization timelines to account for them can have ripple effects across the entire commercialization process, with the potential to impact negatively the likelihood of commercial success or the timeline for that success.

Illustrative Regulatory Pathway Breakdown

- What is the regulatory path that will be taken and why has it been chosen?

- If:

- 510(k)

- What is the predicate?

- What will be the indication for use?

- De Novo

- Will more than just safety data be required?

- How many patients?

- How many years to acquire the data and follow patients?

- What will be the indication for use?

- What special controls may be required?

- 510(k)

- PMA

- What is the subject of the clinical trial?

- How many patients?

- How many years to acquire the data and follow patients?

- What will be the indication for use?

- Will Breakthrough Device Designation be sought?

- What could derail the process and what is fallback position if it happens

11. Reimbursement Strategy

An example of inadequate discussion of the company’s reimbursement strategy — even if, in this case, it plans to use an existing pathway.

On the Slide

This slide articulates the reimbursement path that will be pursued, dependent on the type of product and the market it is addressing. It needs to address the type of code that will be sought, the level of payment that can be expected, and the likelihood and timing of a hospital and physician actually getting paid. It is worthwhile also addressing how the company will make sure that the payment level is realized and supported.

For instance, how the company will ensure that hospitals cost the procedure correctly, thereby leading to a proper payment by CMS that at least covers the actual cost of performing the procedure. In addition, if data above and beyond that required for regulatory authorization is going to be required, how will that data be acquired, how much will it cost, and how long will it take.

Many assume that gaining US regulatory authorization is the major milestone required for commercial success. In some cases, this is correct. Where the new technology is not an entirely different way of doing things and where reimbursement codes, payment, and coverage exist already for the similar procedures, FDA authorization is key. Where this is not the situation, the real challenge lies in reimbursement.

Payers, both public and private, are the ultimate determiners of success of a new technology. No matter how great a new technology, it is tough for it to become a standard of care if it must rely on cash-pay patients, because insurance payors will not pay, or receive a paid payment that is less than the cost of performing the procedure. Gaining coverage from public and private payors, especially if the payment rate is competitive with more traditional approaches (meaning pays enough), will allow a new and presumably better technology to compete on its merits, driving patients to request it which in turn will lead hospitals to acquire it, practitioners to use it, and more units being sold and cases being performed.

- If the proposed technology can co-opt existing codes, then:

- State the code, payment level, and the coverage requirements met by predicate products.

- Describe why new product meets the same criteria as existing products.

- Address if there will be “coverage” uncertainty, and if so, the path to achieve coverage.

- If the proposed technology will require a new code, then:

- Describe path to obtaining a code (C-Code, CPT Cat 1, CPT Cat 3, etc).

- Present a range of payment levels that can be expected for physicians and facility. This will impact product pricing.

- Describe timeline for realizing a code, payment, and coverage. Also address the hurdles that may be encountered along the way and how they will be overcome.

12. Development Pipeline

On the Slide

This examples shows a nice combination of regulatory and financial milestones.

Investors want to be part of a journey. They know that no good story happens overnight so be as thorough as possible on the development timeline.

We suggest aiming for a five-year time horizon to show company development and key milestones. Five years offers enough of vision but also somewhat mitigates forecasting errors that only amplify as you move into out years.

Nobody expects a 1.000 batting average on forecasted needs.

- What is it about the technology underlying the initial product (drug or device) that has the potential to turn said technology into a platform, the potential to apply the innovation to clinical areas beyond the proposed first foray?

- What are the next potential applications for the technology (in sequence)?

- What is the market size for each of these applications ?

- What is the incremental development work, clinical work, and time required to realize a revenue stream from this potential?

Focus

Investors want to see focus at the start of a new company. They want a management team that is all in on a singular idea with complete dedication to bringing the first product to market and making it profitable. That said, most investors interested in building a business, and not just flipping their position, want to know that there is something more down the road. While they want to invest initially in a product, they want to know that ultimately their investment and the product that results from it has the potential to lead to a platform with a corresponding increase in value and return on investment.

Optionality

The most important characteristic of a platform is the ability to create new and more value by facilitating exchanges between an ever increasing number of parties. The fundamental architecture behind all platforms essentially is the same: the system is partitioned in a set of “core” competences with low variety and a complementary set of “peripheral” components with high variety.

Provide enough information, guidance, and detail such that your audience knows you are firmly focused on your initial product but understands where this could lead if the initial endeavor is successful.

Impact on Capital Needs

It is important to note additional funds that may be necessary as projections are made. No early-stage investor will think this is the one and only raise. Include timing of raises, cash outlays, and additional requirements. Investors want to see how much more dilution could be in front of them and what to expect. This will not be a surprise to them, so make sure you over-communicate at the start of the relationship.

Example: Intuitive Surgical

Intuitive Surgical went public in 2000 with a product offering addressing gallbladder and gastroesophageal disease but did not find clinical success until its technology was applied to the prostate in 2001. Prostate was the growth engine that drove the rise of Intuitive to become an economic force. Intuitive has since generalized the product offering such that it is applicable to gynecological procedures and cardiac procedures – two areas from which the greatest recent growth in revenue has come – and now in head and neck surgery, throacic surgery, and colorectal surgery. It sold 60 systems in 2002, compared with 431 in 2014. Its systems were used for less than 1,000 procedures in 2002, compared with 540,000 in 2014.

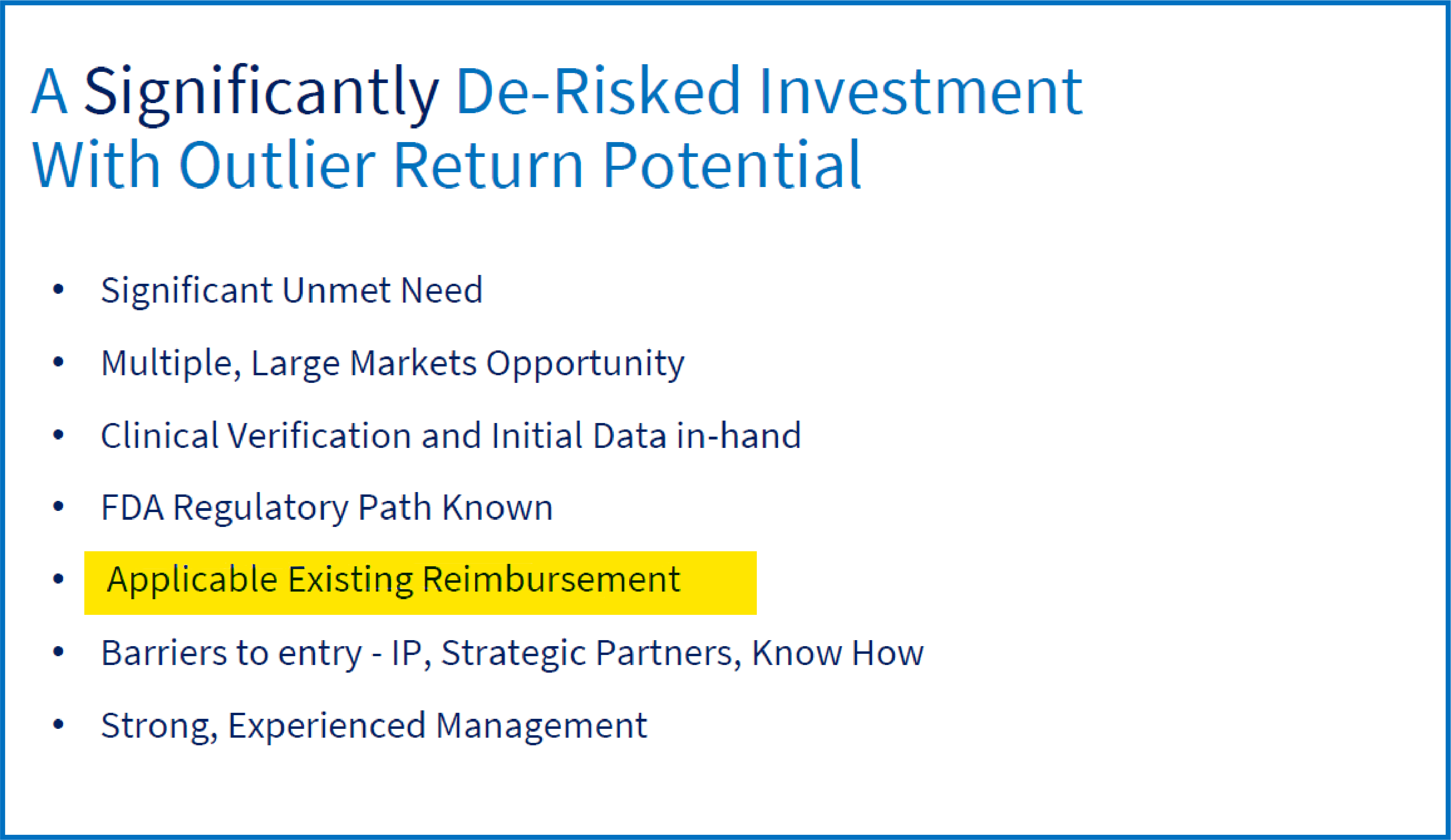

13. Risks

On the Slide

Anyone investing in a startup will have to be an accredited “sophisticated” investor — so they should already be well versed in all the ways they might lose their investment.

Even so, enumerating the particular risks to which your business might be prone can demonstrate important self-awareness while also educating the potential investor to idiosyncratic risks she might otherwise note have contemplated.

Investors want to put money into ventures that have been de-risked as much as possible for their stage. Identifying the risks inherent in any new venture is important in establishing credibility with potential investors and indicating a level of sophistication and reality in the thought process that has gone into developing the business.

So, try to strike a balance between completeness and highlighting those risks that are particular to your business.

As Complete as Possible but Relevant to the Business

While presenting risks does not need to rise to the level included in a formal prospectus, the discussion of risks should be of sufficient detail to demonstrate the thought that has been given to possible remedies or alternative paths to each risk as well as the impact they might have on the overall timeline and cost. Discussing risk can be included in each topic slide or as a dedicated slide devoted to the topic. Think about what can go wrong in each area of focus and make it clear you have thought through how to proceed if such occurs.

Some risks that could be addressed in a medical device deck include:

- What is the possibility the technology will not work or cannot be developed?

- What alternatives exist if the chosen regulatory path is not accepted by the FDA or is unsuccessful in realizing regulatory authorization?

- What happens if there is no payment code or the code is not covered by CMS?

- What if guideline inclusion is delayed for several years resulting in a lack of commercial coverage even in the face of an issued CPT code?

- What happens if a competitor comes along with something better?

- If your company is dependent on creating a new market, what happens if that market fails to develop in the time frame you have projected?

- If your technology works but is not accepted by those in the targeted market, can it be adapted to work in a fallback market?

- If your technology disrupts existing patterns of care, how likely is it that the required new pattern will develop?

14. Summary Financials

On the Slides

The fundraising deck’s intended audience is an investor. They must understand how the success of the business drives the success of an investment. As such, each section of the deck — each page — is an integral part of building the investment case for your business.

The summary financials slide is your opportunity to quantitatively render the elements of the investment case.

Five-Year Proforma Model

Five years is just about the right time frame to sketch out the future of the business you contemplate — not too far out in the future (unreliable) or too close in (an unrealistic time frame to show an investor how they will get a return on their investment). The five year proforma model should show the top-line revenue progression and the resources required to achieve that revenue. The framework is the interlocking income statement, balance sheet, and cash flow statement. The goal is to show (a) the exciting adoption of the company’s products; (b) the extent to which the company can capture the value it is creating; and (c) when the business can achieve cash flow self-sufficiency — or become a very attractive acquisition target.

Key Assumptions

A financial model is only as good as the assumptions behind it. Drawing out those assumptions — and explaining the “what” and the “why” is a great way to show the quality of the thinking behind the business plan. Key assumptions are particular to the business and its financial model. The most important elements are the “why” more than the “what.”

Key assumptions can include financial items (e.g., gross margins, channel margins, sales commissions, and other costs of revenue) as well as market assumptions (e.g., patient populations, condition prevalence, target populations, etc.).

Key assumptions can also include speculation about the timing and type of exit (e.g., initial public offering (IPO), acquisition) and the state of the cap table at acquisition.

All of these assumptions feed into the ultimate outcome for the investor — your target audience.

15. Summary Wrap-up

On the Slide

The summary wrap-up slide should:

- Be a facsimile of the summary highlights slide

- Re-state the investment case you have built for your reader

- Close with the ask (e.g., “We seek $25 million of Series A capital to fund First in Human Trials”)

Make it clear, and don’t worry about being repetitive: tell the reader what you have already told them throughout the deck. Remember, they see 1,500 slide decks each year!